Introduction – Coking Coal:

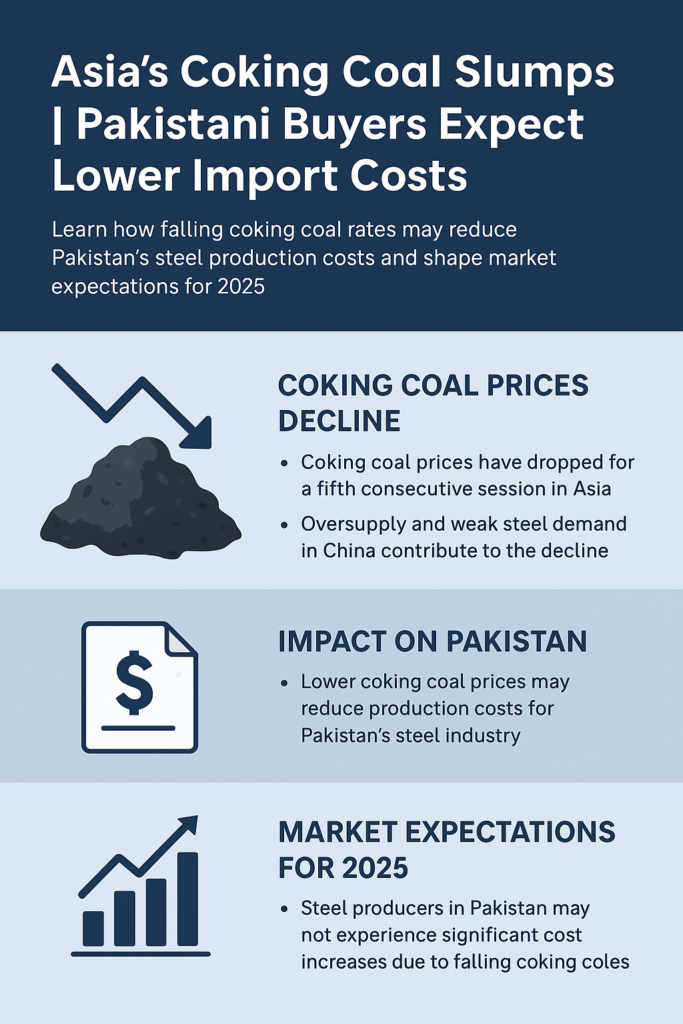

With futures in China declining for the sixth straight day, Asia’s coking coal market is seeing yet another round of downward pressure. Trade expectations are changing throughout the region as a result of this steady drop, especially in places like Pakistan where steel manufacturers mostly depend on imported coking coal. Pakistani steel mills and industrial clients expect lower import expenses in the upcoming weeks as prices continue to decline.

The most recent decline in coking coal prices, its underlying causes, changes in regional supply, and its possible effects on Pakistan’s steel and construction industries are all examined in this article.

Market Overview – Weak Demand Meets Rising Imports:

The Dalian Commodity Exchange saw a 2.4% loss in Chinese coking coal futures, continuing the sharp fall from November. The commodity is on the verge of its worst performance since May, with prices down about 15% this month.

Seasonal demand contraction and a notable rise in import volumes from Australia and Mongolia are the main causes of this downturn.

In blast furnace steelmaking, coking coal is a crucial raw material that is usually used less in the winter. Coking coal is not as urgently needed when steel production decreases as development slows in northern China.

However, this year’s decline is sharper than usual due to stronger import flows.

Go to Zarea immediately, please! to examine the building materials and biomass products, evaluate the costs, and make a sizable buy.

Seasonal Demand Dip in China:

Every winter, China’s construction activity falls due to colder temperatures and reduced on-ground labor operations. This causes steel mills to scale back production, directly reducing coking coal consumption.

The 2025 winter season shows the same pattern:

- Steel demand softens, reducing furnace operations.

- Stockpiles rise, putting downward pressure on procurement.

- Market sentiment weakens, pushing futures lower.

This seasonal trend has coincided with an exceptional increase in imported coal supply, amplifying the market imbalance.

Surge in Australian and Mongolian Coal Supplies:

Australia’s competitive pricing has led Chinese importers to pull in more shipments. At the same time, Mongolia has ramped up export volumes heading into winter.

According to analysts, this dual supply wave is creating a significant supply shock.

Cao Ying, a senior ferrous analyst at SDIC Futures Co., noted:

“Australian coal will directly replenish the coastal market’s high-quality coking coal inventories. Combined with Mongolian coal, this creates a significant supply shock to the domestic coking coal market.”

The impact is clear:

- Australian high-grade coal is filling coastal warehouses.

- Mongolian truck and rail shipments continue to rise.

- Chinese domestic producers are under more pressure from competitors.

As a result, while steel and iron ore have demonstrated relative durability in other Asian markets, benchmark coking coal contracts are currently trading at about 1,100 yuan per ton.

Impact on Coking Coal Prices Across Asia:

The broader Asian market is closely aligned with China’s price movement because China remains the largest importer and influencer of regional sentiment.

Key observations include:

- Lower spot prices across major ports in China, Vietnam, and India.

- Weak procurement activity as steelmakers delay purchases expecting further declines.

- Stable iron ore and steel futures, signaling that coal is under uniquely intense pressure compared to other raw materials.

For Asian buyers, especially emerging markets like Pakistan, this downturn creates an opportunity to reduce costs in an otherwise inflationary economic environment.

What This Means for Pakistan’s Steel Industry

Pakistan heavily depends on imported coking coal for blast furnace and steel production, particularly for long steel products used in construction. The recent decline in Asian prices is likely to benefit the local industry in multiple ways:

Reduced Import Prices

Pakistani steel mills will probably experience lower procurement expenses because global coking coal prices decline. It also relieves pressure on production expenditures.

Possible Consistency in Rebar Prices

The cost of raw materials and currency variations have caused price volatility for steel rebar in Pakistan. In the upcoming months, price stability may be supported by declining metallurgical coal costs.

Improved Margins for Steelmakers

Producers operating on thin margins may experience temporary relief as input costs decline.

Improved Scheduling for the 2025 Building Season

Lower steel prices before the next demand cycle could help Pakistan’s building and development industry if prices continue to be under pressure.

Risks and Uncertainties to Monitor:

Although the market is currently entering a bearish trend. Yet several variables could shift the price direction in early 2025:

- China’s steel policy interventions

- Australian export disruptions due to weather

- Geopolitical shifts in Mongolia-China border logistics

- Currency pressures impacting Pakistan’s import affordability

- Energy costs for local steel production

Pakistani buyers must monitor these factors closely. This is because they can influence import contracts for Q1 and Q2 of 2025.

Outlook – Will Coking Coal Continue to Fall?

Due to low demand and plenty of supply, the majority of economists predict that prices will continue to be under pressure throughout the winter. But once China’s building season returns in the early spring, the market might stabilize.

For now, the trend is clear:

- Prices are falling

- Demand is weak

- Imports are rising

This alignment suggests a window of opportunity for Pakistani consumers looking to obtain cheaper shipments of coking coal.

Final Thoughts:

The ongoing drop in coking coal prices in Asia affects expectations in regional markets that are changing. Meanwhile Australia’s and Mongolia’s high shipments are along with China’s seasonal slowdown. It could have created a supply-heavy situation which lowers prices.

This offers Pakistan a chance to reduce import costs and boost steel production margins. It’s also possible to stabilize building materials costs. In order to plan the best procurement then strategy, buyers, traders, and industrial stakeholders must move forward. They will also need to keep an eye on these market signals as 2025 draws nearer.

If the current trend continues in the same way, then Pakistani steel mills could soon profit from the most competitive coking coal prices in months.